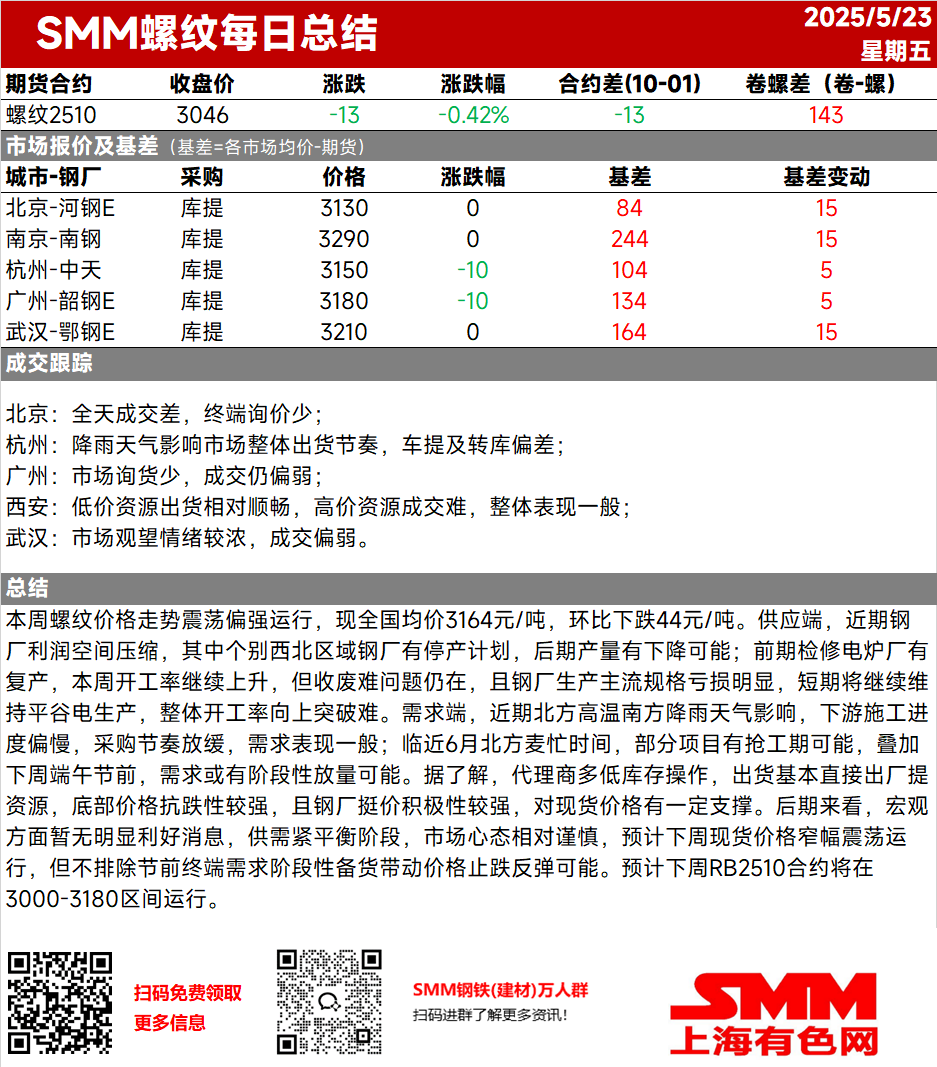

This week, rebar prices fluctuated upward, with the current nationwide average price at 3,164 yuan/mt, down 44 yuan/mt WoW.

On the supply side, steel mills' profit margins have recently narrowed, with some steel mills in the north-west China planning to halt production, suggesting a potential decline in output in the future. EAF steel mills that underwent maintenance earlier have resumed production, and the operating rate continued to rise this week. However, the challenge of scrap collection persists, and steel mills are experiencing significant losses in producing mainstream specifications, leading them to continue operating at off-peak electricity rates in the short term. Overall, it is difficult for the operating rate to break through upwards. On the demand side, influenced by recent high temperatures in the north and rainy weather in the south, downstream construction progress has been slow, and procurement pace has slowed down, resulting in average demand performance. As the wheat harvest season approaches in the north in June, some projects may rush to meet deadlines. Additionally, ahead of the Dragon Boat Festival next week, there may be a phased increase in demand. It is understood that agents are mostly operating with low inventory levels, with goods shipped directly from the mills, indicating strong resistance to price drops at the bottom. Moreover, steel mills are actively refusing to budge on prices, providing some support to spot prices. Looking ahead, there are currently no significant positive macroeconomic signals. With the market in a phase of tight supply and demand balance, market sentiment remains relatively cautious. It is expected that spot prices will fluctuate rangebound next week, but there is a possibility of prices stopping falling and beginning to rebound due to phased stockpiling by end-users ahead of the festival. It is projected that the RB2510 contract will trade within the 3,000-3,180 range next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)